Vanadium Outlook

RECENT NEWS RELEASES

June 7, 2016

American Vanadium Announces Director Nominees for Annual General and Special Meeting

May 24, 2016

American Vanadium Announces Update on Letter of Intent

January 15, 2016

American Vanadium Announces Consulting Agreement and Closing of Previously Announced Private Placement

January 11, 2016

American Vanadium Enters Into a Letter of Intent to Acquire the Complete CellCube Vanadium Flow Battery Business From DMG MORI

October 20, 2015

American Vanadium Announces MTA Installation Date

August 31, 2015

American Vanadium Announces Private Placement

June 8, 2015

American Vanadium Re-Engages Public Relations Firm, Vorticom, Inc.

In its elemental form, vanadium is a soft, silvery gray mineral that's classified as a ductile transition metal. In its various market applications, vanadium represents a billion dollar industry.

And that industry is growing, thanks to the ongoing emergence of new vanadium market applications, and the expansion of conventional applications, particularly in the BRIC countries.

With global vanadium demand projected to more than double by 2025,1 the outlook for vanadium points to increasing consumption across market segments and international boundaries.

Vanadium Production & Uses

Vanadium is produced as a by-product of steel smelter slag, and is also mined in two different types of mineral deposits: disseminated in carbon rich deposits and shales (as with American Vanadium's Gibellini Project), and in magnetite (iron oxide) deposits alongside titanium.

The three largest vanadium producers are China, South Africa and Russia. In North America, vanadium production comes from spent catalyst, residues from burning coal and heavy oil, byproduct of uranium mining, and imported pig iron slag.

With no currently operating primary vanadium mines in North America, and no primary vanadium mining in the U.S. since the 1980s, American Vanadium's Gibellini Project represents the opportunity to become North America's first and only primary producer of vanadium while meeting approximately 5% of current global vanadium demand.

Conventional and new vanadium applications include such diversified industry segments as steelmaking, grid scale renewable energy storage, high performance batteries, catalysts and chemicals.

While the general vanadium market outlook for each of these industry segments is outlined below, in-depth treatments can also be found on the segment-specific pages within this section of the website.

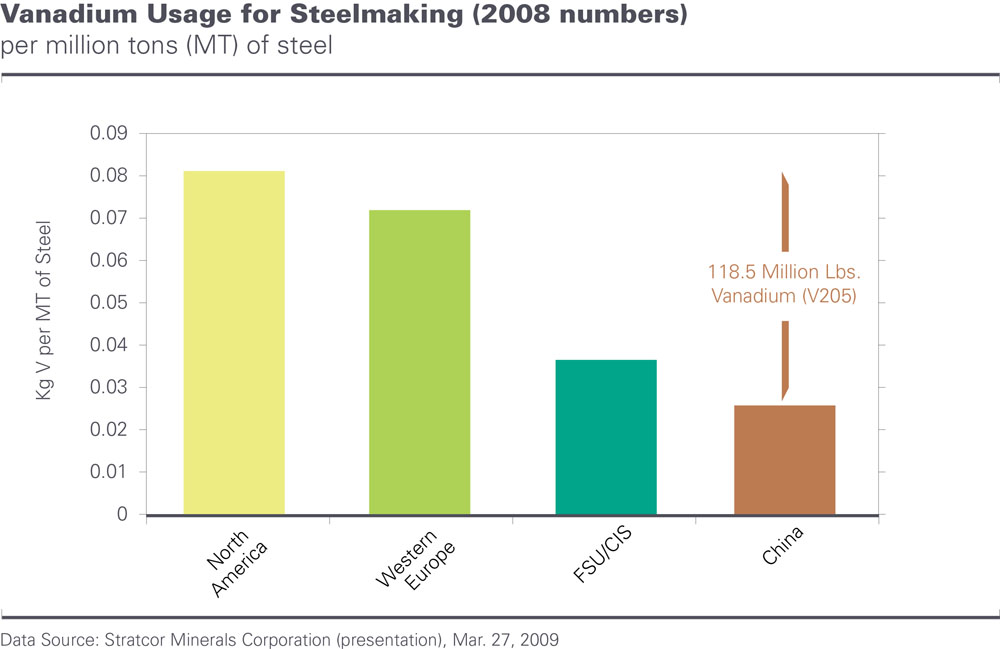

Steel Segment Outlook

When a very small amount of vanadium is added to steel, high-strength low-alloy vanadium steel is created while greatly reducing energy, shipping and production costs.

And while steelmaking accounts for roughly 92% of all vanadium currently consumed, it's estimated that vanadium is only used in about 9% of all steels today.1

That percentage is expected to grow as emerging economies, particularly in the BRIC countries and Asia, increase their intensity of vanadium use in steels to build new infrastructure (e.g., in 2008, intensity of vanadium use in the U.S. was over 3 times that in China).2

International metals consultancy TTP Squared, Inc. forecasts steel-specific vanadium consumption will grow at a Consolidated Annual Growth Rate (CAGR) of 4.8% over the period 2010 to 2025, with over 80% of growth occurring in BRIC countries.1

China's demand for vanadium has already demonstrated substantial growth, with consumption increasing at 13% per year between 2003 and 2009 in line with its surging steel output.2

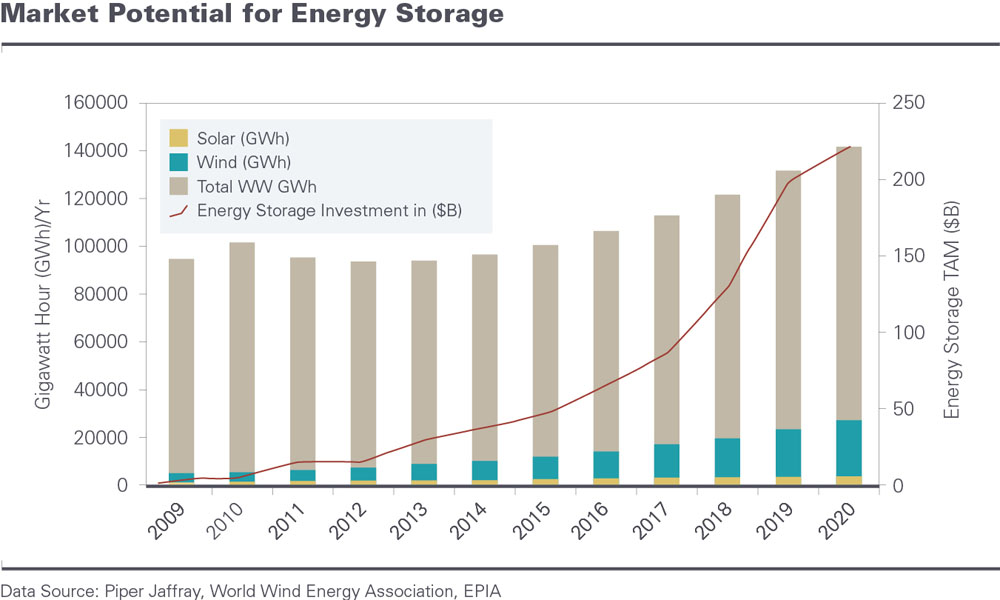

Energy Storage Segment Outlook

In Q1 2011, President Obama gave a speech in Ohio underscoring the need for America to retool and reinvent itself for new industries.

The U.S. government is supporting some of those new industries through investments in renewable energy. In total, $185 million has been set aside to invest in deploying and demonstrating the effectiveness of utility-scale grid storage systems.3

Dwarfing that investment is the ~$600+ billion of industry spending on energy storage solutions that is expected over the next 10-12 years, reaching $200+ billion in 2020 alone.4

And leading the way in new grid scale renewable energy storage solutions are Vanadium Flow Batteries (VFBs). By combining VFBs with renewables such as wind and solar, inherently intermittent energy supplies can be regulated from moment to moment, allowing the grid to balance the amount of energy being put into the wires with the demand arising from consumers.5

Back in Ohio, Obama outlined how Ashlawn Energy had received funding from the Department of Energy's Smart Grid Program, poising that company to manufacture next-generation, multi-megawatt Vanadium Flow Battery energy storage solutions.6

Catalysts & Chemicals Segment Outlook

After steelmaking, the second largest market for vanadium is that of catalysts and chemical applications.

While currently representing up to 5% of global consumption, demand from this segment is projected to grow in the short- and mid-term, according to the leading international metals and minerals research firm Roskill.

In particular, greater demand is expected in connection with the reduction of emissions from coal-fired power plants in developing economies such as China and India,2 as well as emissions from vehicles via catalytic converters.7

Increased consumption is also expected in connection with the production of industry-vital sulfuric acid.2 Among sulfuric acid's many uses is its central role in refining ores containing in-demand 'rare earth metals' that are crucial to new clean technologies.8

Overall Vanadium Market Outlook

Global vanadium demand for 2010 is projected at 61,000 metric tons (MTV), which would exceed former demand highs last seen in 2007.1

According to a Q4 2009 report by Byron Capital Markets, conventional demand for vanadium (primarily from the steel industry) is projected to combine with new market demand, resulting in an overall consumption increase of over 70% between 2009's levels and those of 2014.9

And by 2025, vanadium consumption from steelmaking alone is expected to have increased to roughly 123,000 MTV, which is just over double 2010's global projected demand levels.1

Meanwhile, significant new sources of demand for vanadium are also expected to originate from lithium-vanadium phosphate batteries.

While this new energy storage technology is still considered cutting edge, it continues to impress multiple commercial markets, particularly the automotive industry, where lithium-vanadium phosphate batteries represent the only battery solution with high enough energy density to convince consumers that electric vehicles can compete with gas vehicles on a performance basis.

More Vanadium Market Application Info

As mentioned above, in-depth treatments of each of these vanadium industry segments can be found on the segment-specific pages within this website section:

1. Vanadium Market Fundamentals And Implications. Terry Perles/TTP Squared, Inc., Nov. 16, 2010

2. Roskill's Vanadium: Global Industry Markets and Outlook 2010 report

3. Energy Storage R&D at the U.S. Department of Energy (presentation), June 28, 2010

4. The Metamorphosis of Flow Batteries (Primus Power Corp presentation), June 16, 2010

5. The Element That Could Change the World. Discover Magazine, Sept. 29, 2008

6. Official Whitehouse website (whitehouse.gov), Feb. 22, 2011

7. Global Emissions Management - Volume 2, Issue 12 Spring 2010 (Johnson Matthey)

8. New York Times website, Jan. 20, 2011

9. Vanadium: The Supercharger. Byron Capital Markets report, Nov. 12, 2009